IRS Tax Brackets 2026: New Income Thresholds and Standard Deduction Increases Announced.The Internal Revenue Service has unveiled new federal income tax brackets for 2026. The announcement, made on Thursday, increases the income thresholds for all seven tax brackets. This change is designed to adjust for inflation and will apply to tax returns filed in 2027.These annual adjustments prevent “bracket creep,” where inflation pushes taxpayers into higher brackets without an actual increase in real income. The move provides a measure of financial relief for American households.

A Detailed Look at the New Tax Brackets

The highest tax rate of 37% will now apply to single filers with taxable incomes above $640,600. For married couples filing jointly, the 37% bracket starts at $768,700. This information was confirmed in the official IRS release on tax year adjustments.The new brackets create a slightly wider income range for each tax rate. For example, the 22% rate now applies to single filers earning over $50,400, up from the previous threshold. These adjustments are calculated based on inflation data.

Standard Deductions See a Significant Boost

Standard deductions have also been raised significantly. For single taxpayers, the standard deduction is now $16,100. Married couples filing jointly will see a standard deduction of $32,200.This increase of approximately 2.2% means more income is shielded from federal taxes. According to reports from News Nation, this directly lowers taxable income for the vast majority of filers. It simplifies the filing process for those who do not itemize their deductions.The combined effect of higher bracket thresholds and a larger standard deduction puts more money back in taxpayers’ pockets. It effectively increases take-home pay for millions of Americans.

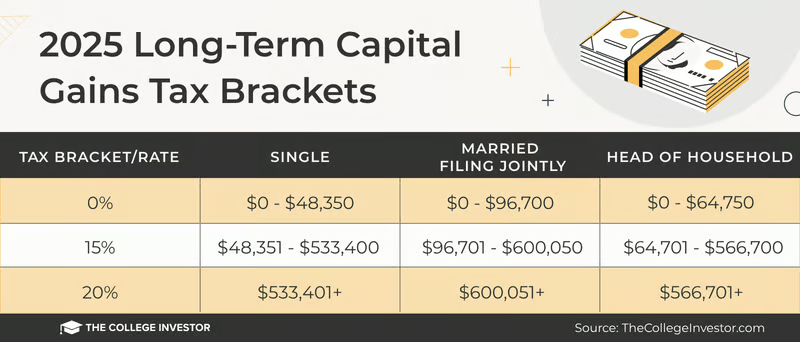

Capital Gains and Other Key Adjustments

Long-term capital gains brackets have also been modified. Single filers with an income up to $49,450 will pay a 0% rate on long-term gains. The threshold for married couples is now $98,900, as reported by CNBC.Estate tax exemptions and earned income tax credit parameters were also updated. These comprehensive changes reflect the IRS’s mandate to annually adjust tax provisions for inflation. The updates ensure the tax code maintains its progressivity.

The newly adjusted IRS tax brackets for 2026 offer widespread relief by accounting for inflation-driven wage growth. These changes will directly impact the financial planning of individuals and families across the United States.

Thought you’d like to know-

What are the new income limits for the 37% tax bracket?

The 37% bracket now starts at $640,600 for single filers. For married couples filing jointly, the threshold is $768,700 in taxable income.

How much has the standard deduction increased?

The standard deduction rose by about 2.2%. It is now $16,100 for single filers and $32,200 for married couples filing jointly.

When do these new tax brackets take effect?

These brackets apply to the 2026 tax year. Taxpayers will use them when they file their returns in early 2027.

What is the purpose of adjusting tax brackets?

Annual adjustments account for inflation. This prevents taxpayers from moving into a higher tax bracket solely due to cost-of-living wage increases.

Have capital gains tax brackets changed?

Yes. The 0% long-term capital gains rate now applies to single filers with income up to $49,450. The limit is $98,900 for married couples.

iNews covers the latest and most impactful stories across

entertainment,

business,

sports,

politics, and

technology,

from AI breakthroughs to major global developments. Stay updated with the trends shaping our world. For news tips, editorial feedback, or professional inquiries, please email us at

[email protected].

Get the latest news and Breaking News first by following us on

Google News,

Twitter,

Facebook,

Telegram

, and subscribe to our

YouTube channel.